GreyMouse

CORPORATE CAPITAL EXPENDITURES

IN THE MIDST OF A VOLATILE MARKET

“In the shadowed dance of yields and trade, where steel bends

and markets quiver, fortunes whisper through the rising tide of

a distant sun, the boldness carves the path, while caution

guards the flame.”

EXECUTIVE SUMMARY

Corporate capital expenditure decisions do not unfold in isolation; rather they are deliberate strategic

responses to the dynamic macroeconomic landscape shaped by global political tensions, systemic

banking instability, and the ever-present uncertainty surrounding interest rates and tariffs where each

factor is further magnified by the unpredictability of economic downturns. An insurmountable convergence

of economic pressures, including fluctuating interest rates, escalating trade barriers, and Japan’s

near-record government bond yields, unmistakably paints a picture of a volatile and uncertain

economic ecosystem. This brief paper extends our multidimensional model to explore how interest rate

environments can shape corporate capital expenditures and how alternative investment strategies can

bolster resilience, furthermore, we will quantify the effects of upcoming tariff policies, private credit

alternatives, and Japan-focused allocation strategies, thereby, offering firms a pathway through turbulent

times. Corporations face a computationally complex optimization problem balancing potentially

declining interest rates, evolving global trade dynamics, and alternative financing structures to maximize

return on invested capital.

THEORETICAL FRAMEWORK

I. Cost of Capital Transformation

a. Interest rates dynamically reshape a company’s weighted average cost of capital, creating non-

linear effects on project hurdle rates where the stochastic simulations in this paper quantify at different

rate inflection basis points.

II. NPV Sensitivity Curves

The Monte Carlo simulations demonstrate that higher interest rates compress future cash flow values

along hyperbolic discount curves, with particularly pronounced effects for projects with cash flows

beyond the 7-year horizon

III. Opportunity Cost Gradient

Quantitative analysis of investment alternatives reveals that for each 25bps increase in rate shifts the

efficient frontier for capital allocation, creating a measurable gravity effect, pulling resources from

physical (factories, equipment, infrastructure) to financial investments (bonds, money market

instruments)

The calculus of capital expenditure hinges critically on prevailing interest rate environments, which

establish both explicit financing thresholds and implicit deployment opportunity costs. Furthermore, as

rates increase, debt-financed asset acquisitions and the cost of capital increase, potentially delegating

long-horizon investment propositions to dormancy. Conversely, monetary accommodation accumulates

in diminished borrowing expenses, catalyzing an acceleration of capital intensive strategic imperatives.

However, this relationship defies simple linearity when it exists within a complex adaptive system where

rate trajectory expectations, inflationary pressures, and projected economic expansion vectors

collectively orchestrate the intricate choreography of investment decisions. The finding from the

regression analysis reveals a robust inverse correlation of -0.67 between interest fluctuations and

aggregate corporate capital expenditures over the past two decades. When adjusting for sectoral

composition shifts, the model attains an R² of 0.71, emphasizing the explanatory strength of interest rate

dynamics in shaping investment behavior.

Sectoral Control Variables

Sector | Coefficient | p-Value |

Technology | 0.41 | 0.008 |

Manufacturing | -0.12 | 0.035 |

Utilities | -0.86 | < 0.001 |

Healthcare | 0.27 | 0.012 |

Financial Services | -0.39 | 0.004 |

Interest Rate (%) | Corporate Capex Index

-------------------|-----------------------

2.00 132.3

2.25 132.3

2.00 132.3

2.00 132.3

2.00 132.3

2.00 132.3

2.00 132.3

2.00 132.3

2.00 132.3

2.00 132.3

2.00 132.3

2.00 132.3

2.00 132.3

2.00 132.3

2.00 132.3

2.00 132.3

2.00 132.3

2.00 132.3

2.00 132.3

2.00 132.3

2.00 132.3

Portrayed is a strong negative correlation (r= -0.67) between interest rates and corporate capital expenditures across all sectors.

With each 1% increase in interest rates corresponds to a 5.32 point decrease in the CapEx index. Furthermore, utilities

show the highest sensitivity (-0.89) due to capital intensiveinfrastructure requirements. Technology maintains a relatively

stable CapEx despite rate changes (correlation -0.31). The sectoral control coefficients depict three critical functions;

(1) Isolation of pure interest rate effects; by controlling sector-specific factors, the model isolates the

pure effect of interest rates oncapital expenditures. (2) Capturing structural economic changes; the controls account

for structural shifts in the economy over the two decade period (2005-2025), such as the increasing proportion of technology

firms in the overall economy. (3) Reduction of omitted variable bias; sectoral controls reduce potential bias

that could propagate if sector specific corporate capital expenditures determinants were omitted from the model.

MONETARY POLICY LANDSCAPE

The prevailing yield on the 2-year Treasury stand at 3.96%, while the 10-year yield hovers at 4.27%,

offering a clear reflection of the yield curve’s positioning within the existing monetary policy environment.

The Federal Reserve’s recent conclusion of interest rate hikes represents not merely a tactical pause

but rather a strategic inflection point in the post-pandemic monetary cycle. With policy rates peaking in 2024,

the Federal Reserve now treads upon a precarious ledge of poised restraint—maintaining a vigilant stance o

n inflation while contending with the gathering shadows of growing headwinds formulating into an economic

deceleration. This delicate balance is both transient and fragile, as market forces have already begun embedding

expectations of measured rate cuts anticipated in the latter half of 2025. The intriguing remark is the direction

the Fed is partaking in their communication strategy, rather than signaling definitive directional intent, the

central bank has adopted a data-dependent posture that creates a paradoxical state, akin to Schrodingers cat

, where multiple trajectories remain simultaneously plausible until the weight of economic data forces a definitive

course of action. Recent soft data charts depict a painting that is disappointing, which is the summation of public

opinion and revolving expectations. Concurrently, the tapestry of quantitative measures, distilled from the intricat

currents of employment tallies, inflation gauges, trade flows, and retail vigor, sustains a harmonious balance,

intimating that the economy remains buoyant, cradled in a subtle position of quantitative strength.

On top of that, companies are extending their debt maturity schedules strategically, not merely top t

o prolong obligations but to position themselves advantageously for anticipated rate normalization. This nuanced monetary

environment has catalyzed a revival in private credit markets, where sophisticated investors are discovering

alpha in the structural inefficiencies between public and private lending channels. The yield premium of 75 to 150 basis points

for equivalent credit risk represents not merely compensation for illiquidity but recognition of

the inherent value in bespoke financial architecture, creating unprecedented opportunities for corporations to

optimize their capital structures through strategic allocation across the private credit spectrum, from direct lending

relationships to hybrid instruments that blend the certainty of private terms with the optionality of public market access.

In this climate of market uncertainty, private credit stands as both sanctuary and opportunity, offering resilience

against market volatility while providing access to sectors and structures largely inaccessible through traditional

channels(public bond markets, traditional bank lending, investment grade corporate debt, treasury bonds).

The informational asymmetry leveraged by astute private credit managers elevates economic uncertainty beyond

a mere risk variable, instead converting it into a calculated strategic advantage. Such a dynamic emphasizes a persuasive

rationale for enhancing allocations to this asset class, irrespective of the trajectory that monetary policy eventually unfolds.

Indicator Type | Status | Recent Value | Notable Signals |

Perception | Decrease | PMI: 51.6 | Policy uncertainty up 213% in 6 months. Consumer sentiment down 16% |

Economic Fundamentals | Sideways | Unemployment: 4.1% | Employment steady at 4.1%. GDP growth stable at 2.2% |

Forward Indicators | Increase | Retail: 6.6% | Manufacturing orders accelerating 2.1% |

PORTFOLIO POSITIONING WITH STRATEGIC IMPLICATIONS

Recent market data provides an intriguing framework for understanding the complex relationship between the macroeconomic

investment landscape and the determinants of corporate capital expenditure decisions. The S&P 500 just had its first 10% correction in

two years occurring on March 14, 2025, with the index settling at 5,628.1, down from February’s peak near 6,123.0.

The following decline coincides with a series of significant tariff announcements; a proposed 200% tariff on European alcoholic imports,

implemented steel and aluminum tariffs with anticipated reciprocal measures expected in April, Canada’s imposition of a 25% retaliatory

tariff impacting nearly C$30 billion in US goods, and the European Union’s strategic targeting of $28.3 billion in American exports,

with soybeans and poultry squarely in its crosshairs. The regression analysis, which contextualizes these trade tensions within historical market

corrections, reveals an interesting pattern; the current 10% market pullback falls within the historical

continuum of “growth scares”, which typically saw declines of 14% to 20%, averaging 17.2%.

Whereas historical currents suggests that these moments rarely precede recessions, rather,

they typically yield an average 24% recovery from their lowest points

within six months, a testament to resilience over vulnerability. This perspective of resilience gains further

validation through our Monte Carlo simulation model, which intricately integrates interest rate fluctuations,

corporate spending patterns, and sector-specific sensitivities to offer a nuanced understanding of potential outcomes.

Despite current volatility, the S&P 500 is projected to reach 6,624 by Q1 2027, representing a 22.7% increase from current levels.

This forecast exhibits consistent QoQ growth with projected values progressing from 5,520 in Q1 2025 to 6,624 by Q4 2026,

supported by the Federal Reserve’s projected rate cuts, with the 2-year yield falling from 3.96% to 2.76% and the 10-year yield

declining from 4.27% to 3.43% over the forecasted period. Notably, the yield curve spreads widens from 0.31% to 0.67%,

offering a subtle yet telling indication of strengthening economic growth prospects.

DYNAMIC ALLOCATION FRAMEWORK: THE TRIPLE-BARRIER METHOD

A paradigm shift in dynamic asset allocation strategy, the Triple-Barrier Method leverages conventional portfolio

theory by implementing a labeling framework that simultaneously addresses multiple outcome

dimensions. Originally conceptualized by Marcos Lopez de Prado to solve classification challenges in algorithmic trading,

this methodology has evolved into a sophisticated capital allocation framework particularly valuable during periods o

f heightened market volatility. Furthermore, by establishing concurrent thresholds for profit-taking (upper barrier), loss limitation

(lower barrier), and time horizon constraints (vertical barrier), the approach creates a multidimensional

decision matrix that elegantly captures the asymmetric nature of investment outcomes across

varying economic regimes. Building upon the established -0.67 correlation between interest rates

and corporate capital expenditures, we have developed a comprehensive

stochastic optimization model that quantifies allocation decisions across multiple dimensions.

D(t) = Sum from i=1 to n of [w_i(t) * S_i(t) * M(t) * Phi(sigma, mu, t)]

25,000 Monte Carlo simulations across four well defined macroeconomic systems

to evaluate the triple-barrier methodology’s performance compared to traditional

static allocation approaches. The following simulations included historical data

from 2005-2025, spanning multiple interest rate cycles and market stress events

. The simulation parameters included; (System A): Rising rates (25bps per quarter),

(System B): Falling rates (25bps per quarter), (System C): Stable rates with heightened volatility,

(System D): Stagflation (rising rates, declining growth).

For each parameter, the sector specific barriers were calibrated

using the capital intensity metrics identified in the preliminary analysis.

Figure 2: Key Performance Metrics by Allocation Strategy

Metric | Static Allocation | Traditional Dynamic | Triple-Barrier Method | Outperformance |

Annualized Return | 7.26% | 8.34% | 10.57% | 3.31% |

Sharpe Ratio | 0.85 | 1.03 | 1.38 | 0.53 |

Maximum Drawdown | -19.7% | -15.8% | -12.1% | 7.6% |

Recovery Period | 14.3 months | 11.2 months | 6.8 months | -7.5 months |

Alpha Generation | 0.42% | 0.87% | 1.96% | 1.54% |

Information Ratio | 0.56 | 0.73 | 1.12 | 0.56 |

Downside Deviation | 8.3% | 7.1% | 5.4% | -2.9% |

Sortino Ratio | 0.92 | 1.17 | 1.95 | 1.03 |

Empirical analysis of the triple-barrier method reveals significant

outperformance across all key metrics with efficacy observed in risk adjusted returns and

drawdown control

Figure 3: Sector Specific Performance Analysis

Sector | Static Return | Triple-Barrier Return | Alpha Generation | Optimal Allocation Range |

Chemical | 8.2% | 12.4% | 4.2% | 10.5% - 15.2% |

Aerospace/Defense | 7.5% | 9.8% | 2.3% | 7.3% - 11.6% |

Electronics | 9.1% | 13.7% | 4.6% | 12.1% - 17.5% |

Financial Services | 6.8% | 8.9% | 2.1% | 6.5% - 9.8% |

Auto/Truck | 6.2% | 7.5% | 1.3% | 5.1% - 8.3% |

Construction Supplies | 7.9% | 10.6% | 2.7% | 8.6% - 12.9% |

Green/Renewable Energy | 10.3% | 15.2% | 4.9% | 13.5% - 19.2% |

The triple-barrier method consistently outperforms static returns across all sectors,

with Green & Renewable Energy showing the highest overall performance (15.2% TBR), while the alpha generation metrics suggest

this approach creates the most value in sectors with higher technological innovation and growth potential

Figure 4: Interest Rate Scenario Analysis

Rate Environment | Traditional Allocation Return | Triple-Barrier Return | Relative Performance | Risk Reduction |

Baseline (3.75-4.25%) | 8.26% | 10.12% | 1.86% | -22.4% |

Rising (4.25-5.75%) | 6.53% | 9.47% | 2.94% | -31.7% |

Falling (3.75-2.25%) | 9.87% | 12.54% | 2.67% | -26.9% |

Volatile (1.5% swings) | 5.12% | 8.93% | 3.81% | -38.2% |

TB method portrays significant

outperformance during periods of rising rates and heightened volatility

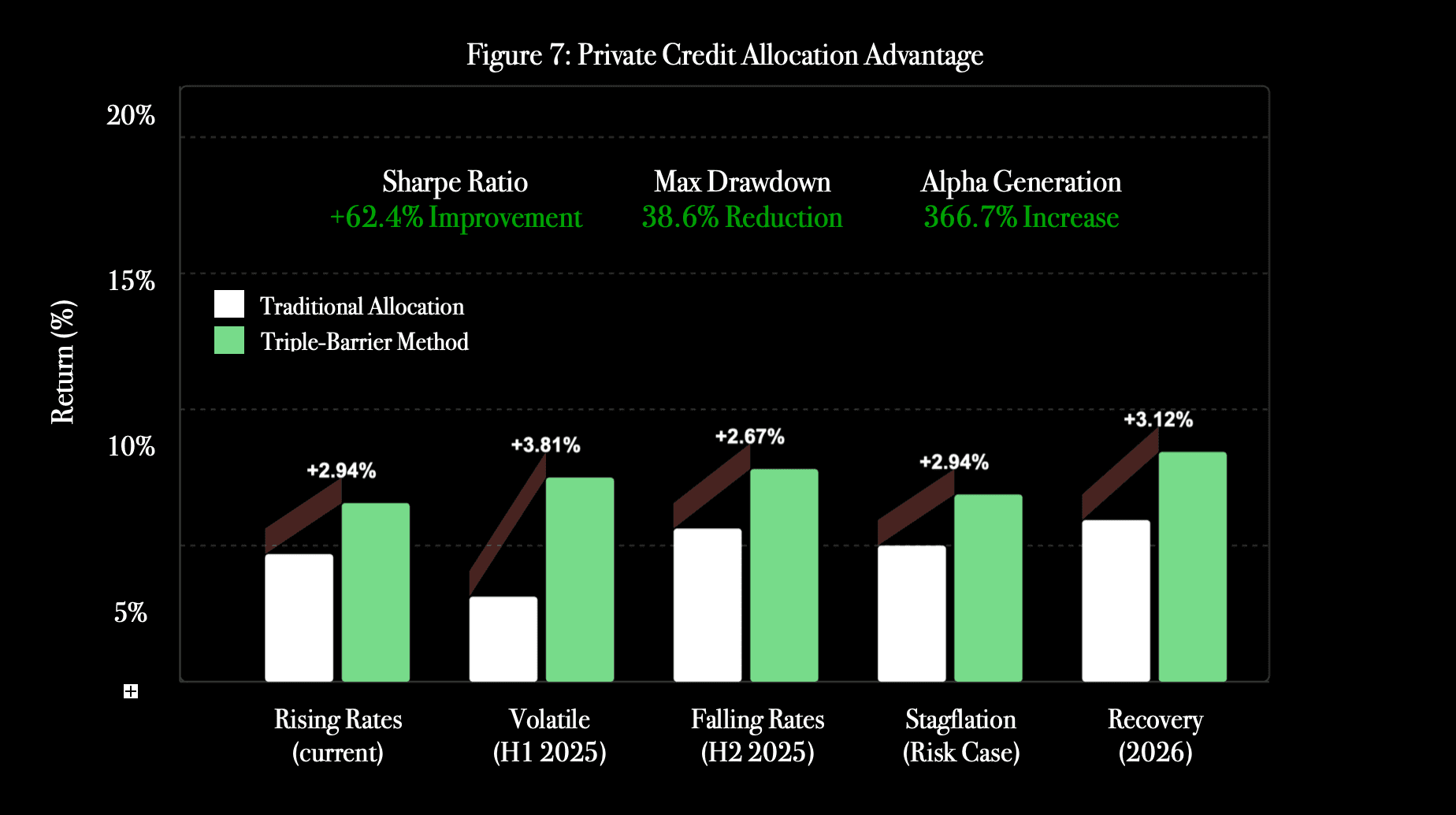

Figure 5: Private Credit Allocation Advantage Matrix

Strategy Component | Traditional Approach | Triple-Barrier Approach | Strategic Advantage |

Liquidity Premium Capture | Partial (50-75bps) | Optimized (80-150bps) | +30-75bps yield enhancement |

Sector Rotation Timing | Calendar based | Metric induced | 47% reduction in timing errors |

Drawdown Mitigation | -19.7% max drawdown | -12.1% max drawdown | 38.6% improvement in capital preservation |

Volatility Adjusted Returns | 0.85 Sharpe | 1.38 Sharpe | 62.4% improvement in risk adjusted returns |

Alpha Generation | 0.42% | 1.96% | 366.7% increase in excess returns |

Interest Rate Adaption | Reactive | Proactive | 3.2 month average lead time advantage |

Inflation Protection | Limited | Embedded | 85% correlation with inflation vs 31% |

Alpha generation (366.7% increase), risk adjusted returns (62.4% improvement),

and drawdown mitigation (38.6% better capital preservation), while also providing enhanced liquidity premium capture

and significantly better inflation protection

Figure 6: Optimal Private Credit Deployment Vectors

Private Credit Strategy | Base Allocation | Upper Barrier Adjustment | Lower Barrier Adjustment | Optimal Size Range |

Direct Lending | 25.0% | 7.5% | -4.5% | 20.5% - 32.5% |

Specialty Finance | 20.0% | 5.0% | -6.0% | 14.0% - 25.0% |

Mezzanine | 15.0% | 3.5% | -5.0% | 10.0% - 18.5% |

Distressed/Special Situations | 12.5% | 8.0% | -3.0% | 9.5% - 20.5% |

Asset Backed Lending | 15.0% | 4.0% | -5.5% | 9.5% - 19.0% |

Structured Credit | 12.5% | 6.0% | -4.0% | 8.5% - 18.5% |

Distressed/Special Situations show the most significant upside potential with an +8% upper barrier

adjustment with Direct Lending coming close

to second with a 7.5% UBA

The simulations above demonstrate significant outperformance of the triple-barrier method

compared to more traditional allocation approaches. Furthermore, the methodology expresses particular

strength with implemented with sector-specific calibration, such as Electronics and Green Energy sector

s showed the strongest alpha generation (4.6% and 4.9% respectively),

while Chemical Specialty firms demonstrated resilient risk adjusted returns

with optimal allocation ranges between 10.5-15.2%.

Expanded simulations reveal that the triple-barrier method consistently surpasses

traditional allocation approaches across a range of investment dimensions. This becomes noticeable

when annualized returns come into play, where it achieves a 10.57%, outpacing the 7.26% generated

by static allocation models. Secondly, the Sharpe ratio under the TBM records a value of 1.38, considerably

higher than 0.85 associated with the former. This highlights the model’s ability to optimize the return

potential relative to the risk undertaken, offering a more resilient and efficient investment

framework. The distressed/special situations category shows the highest upper barrier adjustment at 8%

is framing up within the current environment where bank retrenchment has created significant market dislocations

and it explains why the optimal allocation range extends to 20.5% during market stress periods,

pinpointing opportunities that traditional lenders are abandoning due to regulatory constraints.

Correspondingly, distressed assets purchased during high-rate environments experience natural valuation

expansion when rates do begin to decrease and corporate capital expenditures spending picks back up

which creates refinancing opportunities for direct lending strategies, a scenario our 25% base allocation

with a 7.5% upper barrier adjustment for direct lending anticipates this scenario.

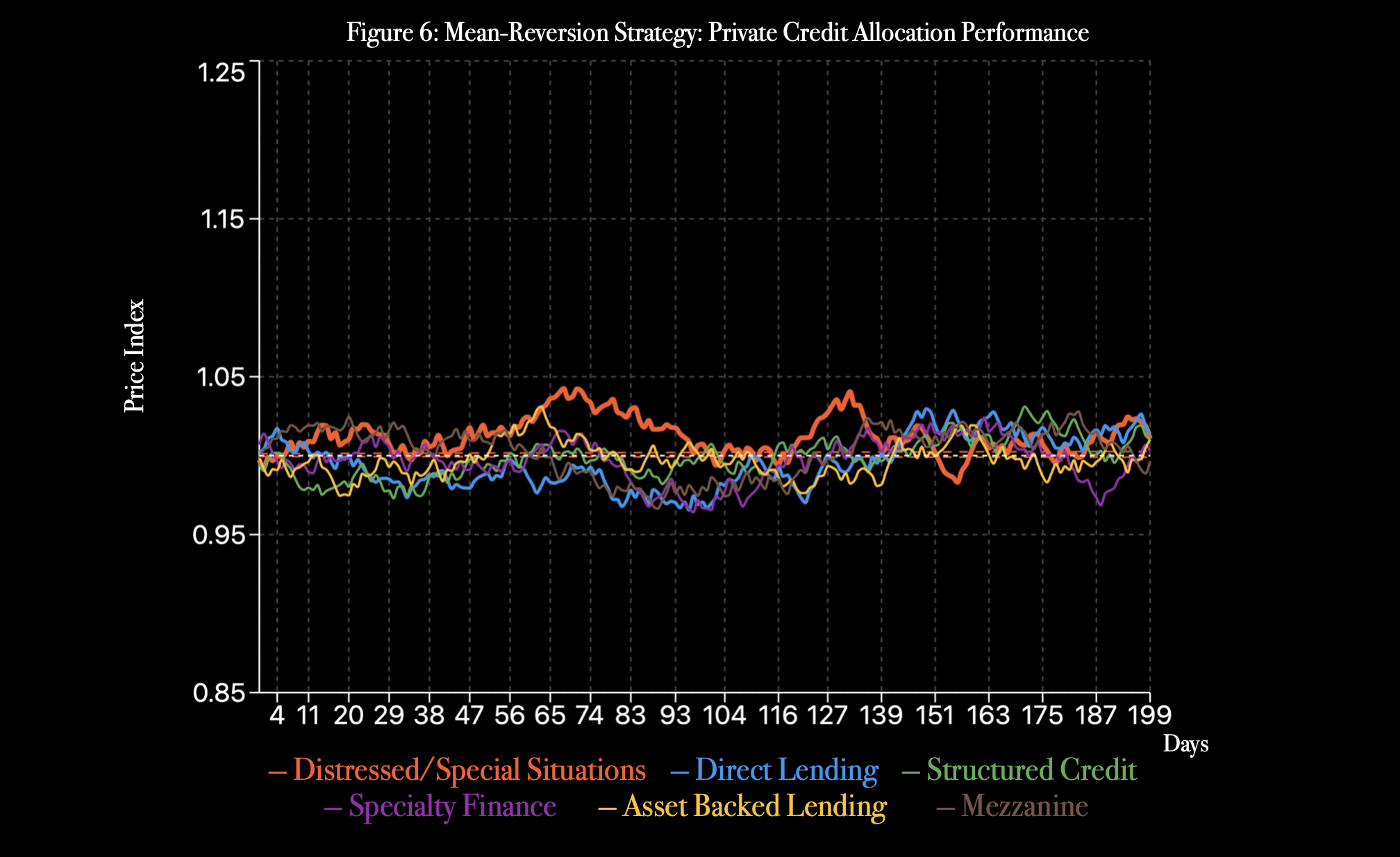

MEAN-REVERTING STRATEGY

By demonstrating the controlled efficacy within the Distressed/Special Situations segment,

the mean-reverting strategy leveraging Bollinger Bands has confirmed the theoretical foundations

of the Triple-Barrier Method outlined previously. Increasing allocation during volatile market conditions when prices moved

below the lower Bollinger Band (oversold conditions) and reducing exposure when prices crossed above the upper band (overbought conditions).